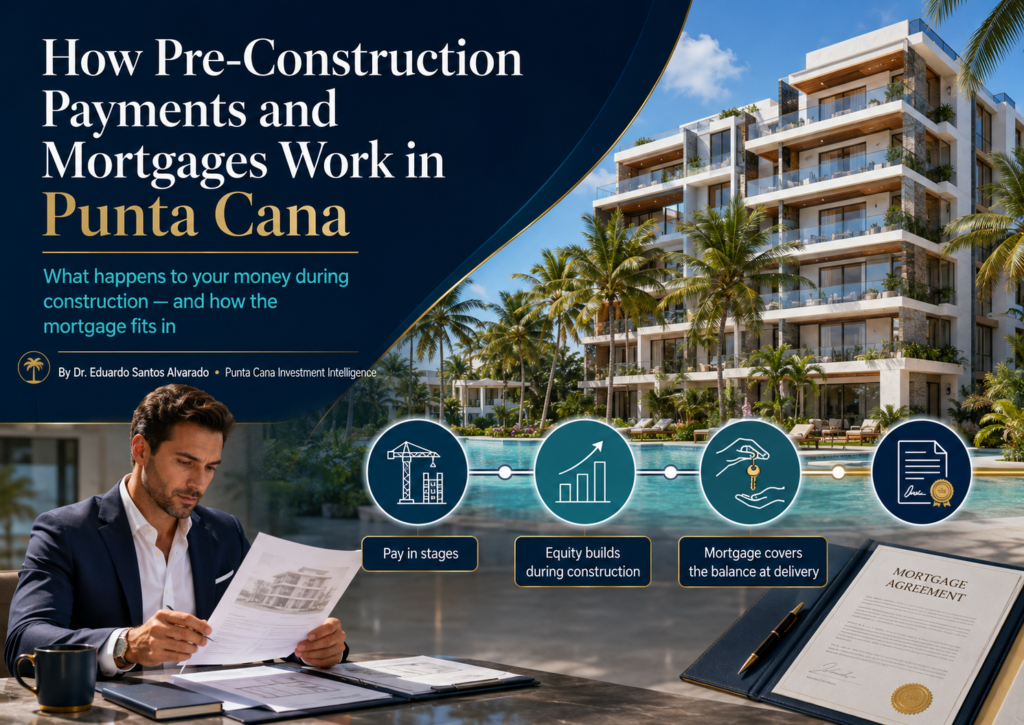

Serious investors don’t ignore risk — they price it. Buyers who approach the Dominican market deliberately tend to weigh distinct categories of risk rather than treat “risk” as one vague worry, and that’s the right instinct. This guide breaks the five that matter most for Punta Cana into plain terms: what each one actually is, how it applies here specifically, and how it can be managed.

None of these is a reason to avoid the market. Each is a reason to go in with your eyes open — and to size your purchase so that no single risk can sink you.

1. Legal & title risk

This is the most consequential risk and, fortunately, the most controllable. The Dominican property system is sound on paper — a registered title system backs ownership — but enforcement gaps, an unregulated brokerage profession, and the absence of common safeguards create room for trouble.

The specific exposures: a seller who doesn’t truly own the property or whose documents are forged; a parcel with no completed deslinde (registered boundary survey), where what you’re buying isn’t legally defined; the same unit sold to more than one buyer; and deposits wired with no protection, since true escrow accounts and title insurance are both uncommon here.

How to manage it. This risk responds almost entirely to process. Engage your own independent attorney, verify the title and boundaries in the Registro Inmobiliario before any money moves, and for preconstruction insist your deposit sits in a fideicomiso (guarantee trust). Our [Punta Cana Real Estate Scams & Red Flags] guide and [Due Diligence Checklist] cover exactly what to verify. Of the five risks here, this is the one you have the most power over.

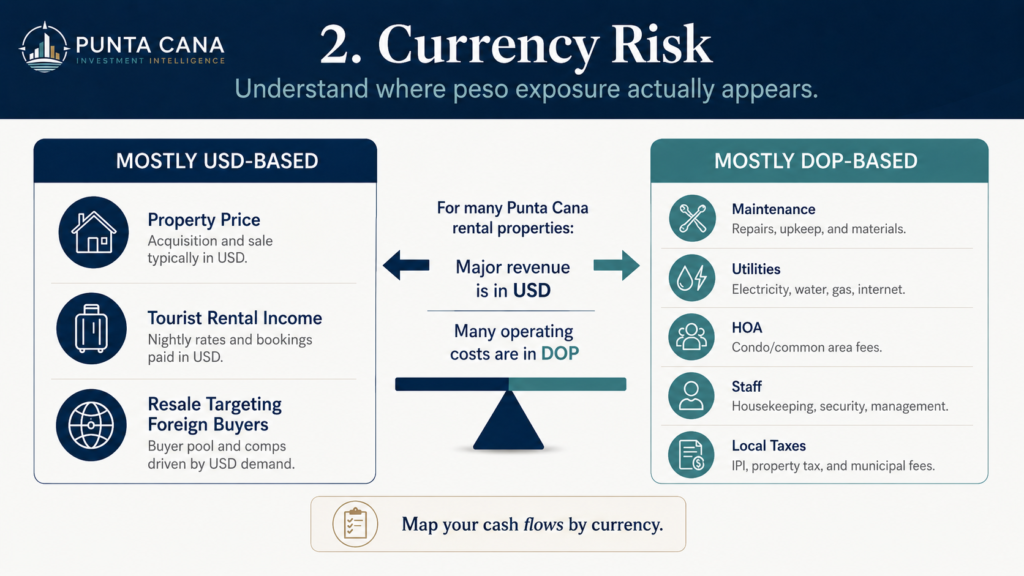

2. Currency risk

The Dominican peso has depreciated against the US dollar over the long run — from roughly 27 per dollar in 2004 to around 58–60 in 2026 — although it has been notably stable, even slightly stronger, over the past couple of years. Inflation runs near 5% and the central bank holds a relatively high benchmark rate, both of which shape the currency’s path.

Here’s the part most foreign buyers get wrong, in their own favor: Punta Cana investment property is overwhelmingly priced, sold, and rented to tourists in US dollars. That means your asset value and your tourist-rental income are effectively dollar-denominated, which insulates you from much of the peso’s movement. Where currency risk actually bites is on the local-cost side — maintenance, staff, utilities, HOA fees, and peso-denominated taxes all sit in DOP.

How to manage it. Map which of your cash flows are in dollars and which are in pesos. A USD-priced asset earning USD rental income carries limited direct currency risk; the exposure is mostly on operating costs, which are a smaller line. Don’t let “currency risk” scare you off — but do understand where it genuinely applies.

3. Liquidity risk

Real estate is illiquid everywhere. In Punta Cana, a few structural features make it more so. There is no centralized MLS, so price discovery and exposure to buyers are fragmented. The resale market is thinner than the primary market and leans on the same pool of foreign buyers, which means selling can take many months — and far longer if the title or deslinde isn’t clean.

How to manage it. Buy with a multi-year horizon, not a quick-flip mindset; this market does not reward investors who need to exit fast. Keep your legal file immaculate, because a property with clean title, a registered deslinde, and current IPI sells dramatically faster than one with paperwork gaps. And budget for the reality that converting the asset back to cash takes time.

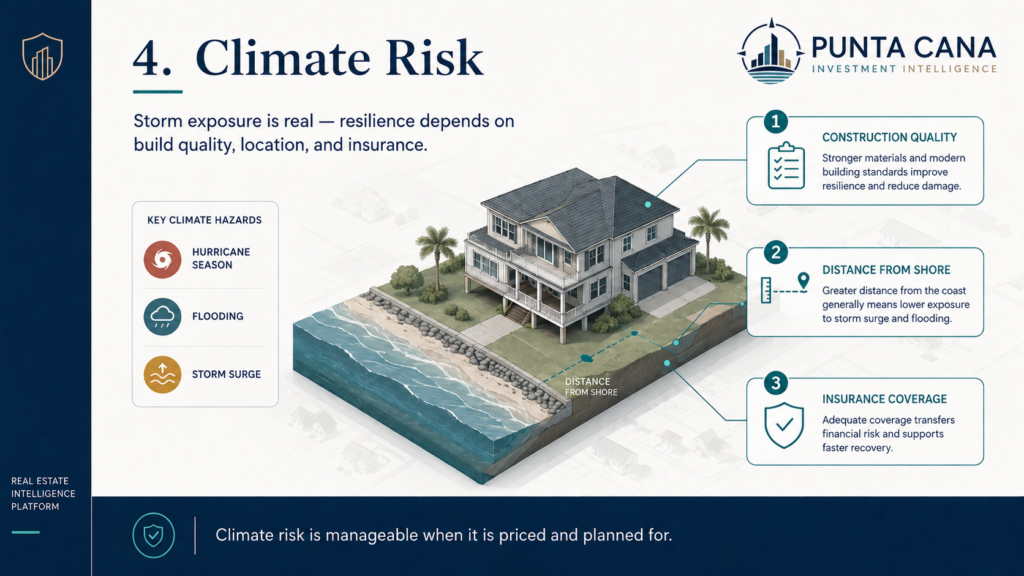

4. Climate risk

The Dominican Republic sits in the Atlantic hurricane belt, with a season running roughly June through November, and Punta Cana is on the country’s exposed east coast. Hurricane Fiona, in September 2022, struck the east, prompted a state of emergency across eight provinces, and briefly closed Punta Cana’s airport. Beyond hurricanes, heavy rain can bring flooding, and coastal proximity adds exposure to storm surge and erosion.

The context matters too: the DR has historically weathered major storms better than several neighboring islands, and natural disasters cost the country on the order of half a percent of GDP per year — meaningful, but not catastrophic at the national level.

How to manage it. Favor well-built, modern, code-compliant construction over cheaper or older builds, since storm damage concentrates in flimsy structures. Confirm what insurance is available and exactly what it covers. And weigh honestly how close to the water you want to be — beachfront carries both the premium and the exposure. Properties within the 60-meter maritime zone also carry their own permitting rules worth checking.

5. Tourism-dependency risk

Punta Cana’s economy is built on tourism to an unusual degree. Its international airport handles roughly 64% of all air arrivals into the entire country, the area holds around 50,000 hotel rooms, and rental demand is driven almost entirely by visitors. The upside is genuine and currently strong: national arrivals hit record highs — around 11.6 million in 2025 — drawn from diversified source markets including the US, Canada, Colombia, Puerto Rico, and Argentina.

The risk is concentration. Because occupancy, rental income, and resale demand all depend on the same single engine, a tourism shock — a pandemic-style halt, a security scare, a broad travel downturn — would hit all three at once. A diversified local economy can absorb a blow to one sector; a tourism monoculture feels it everywhere.

How to manage it. Stress-test your numbers against lower-occupancy scenarios rather than underwriting to peak-season highs. Be clear with yourself that a rental thesis here is, at bottom, a bet on continued tourism growth — a bet that has paid off handsomely in recent years, but a bet nonetheless. Size the purchase so a soft year is survivable, not fatal.

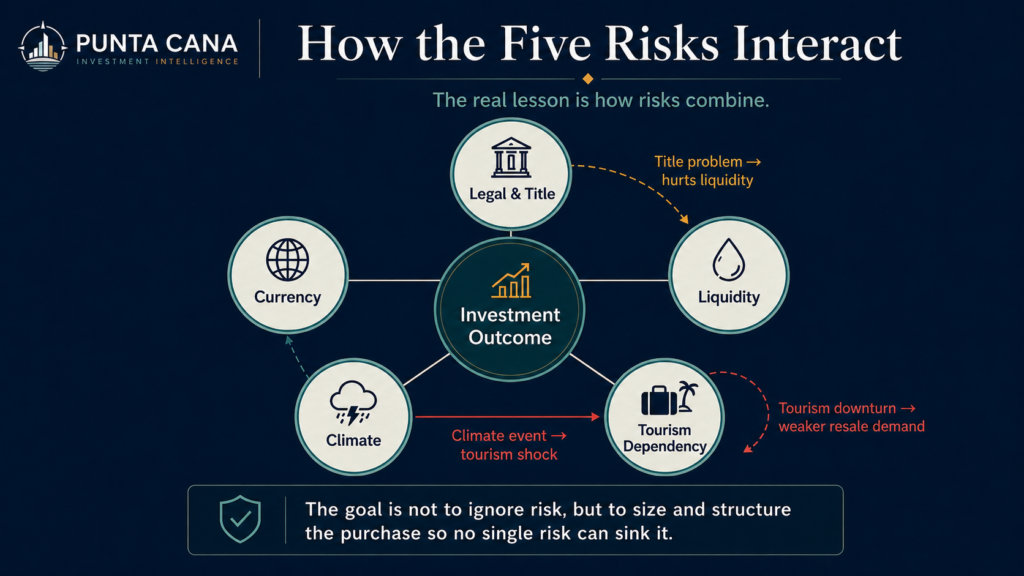

How the five interact

These risks aren’t independent, and that’s the real lesson. A major climate event is also a tourism shock. A tourism downturn deepens liquidity risk by thinning the buyer pool exactly when you might want to sell. A title problem destroys liquidity outright. The goal isn’t to fear any one of them — it’s to structure your purchase, your horizon, and your expectations so that no single risk, or plausible combination, can take you down. That is what separating risk into categories is for.

Frequently asked questions

Is Punta Cana a safe place to invest? For a prepared buyer, yes. The market has real, named risks — but the most consequential one, legal and title risk, is also the most controllable through proper due diligence.

What is the single biggest risk? Legal and title risk — and it’s the most preventable. Most losses trace back to skipped verification, not to market or climate forces.

Does the weak peso hurt foreign investors? Less than many expect. Property is typically priced and rented in US dollars, so your asset and tourist income are largely dollar-based; the peso mainly affects local operating costs.

Are hurricanes a dealbreaker? No, but they’re real. Build quality, location relative to the coast, and insurance coverage are what separate a manageable risk from an expensive one.

How long does it take to sell a property here? Plan for months, not weeks — and keep your title, deslinde, and IPI current, because clean paperwork is the difference between a sale and a stalled listing.

Score a specific deal against these risks → [Run the Real Estate Risk Score] Get the printable checklist → [Download the Due Diligence Checklist]

This guide is educational and does not constitute legal, tax, or financial advice. Market, currency, and climate conditions change. Evaluate any specific purchase with qualified, independent professionals before committing funds.