By Dr. Eduardo Santos Alvarado · Punta Cana Investment Intelligence

If you’ve looked at a pre-construction project in Punta Cana, you’ve seen the payment plan: a little down to reserve, more during construction, and a large balance “at delivery.” It looks simple on the brochure. But one question trips up almost every foreign buyer, and the developer’s sales team rarely explains it clearly: what happens to all the money I pay during construction — and how does the mortgage fit in?

This guide answers exactly that. We are not selling property. The goal is to give you an accurate, plain-English picture of how the money actually moves, so you can plan your cash and your financing with clear eyes.

The typical payment structure

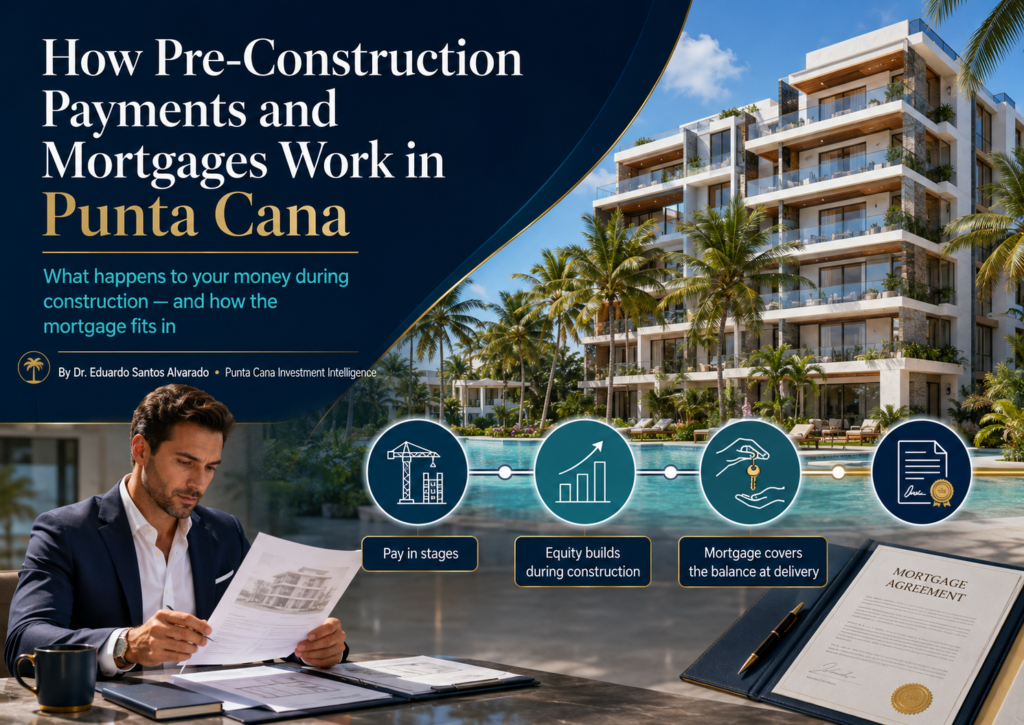

Pre-construction (buying “off-plan,” before the building exists) is paid in stages tied to the construction timeline. The exact split varies by developer and project, but a common pattern in Punta Cana looks like this:

- Reservation — a small upfront amount to take the unit off the market. Sometimes a fixed figure (often in the US$5,000–$10,000 range), sometimes a first slice of the down payment.

- Down payment at signing — you complete your down payment when you sign the purchase contract, frequently around 20% of the price.

- Installments during construction — you pay scheduled amounts as the building goes up, until your total paid reaches somewhere between 30% and 50% by the time the project is delivered.

- Balance at delivery — the remaining 50% to 70% is due when the developer hands you the keys (“a la llave”).

Some developers ask for a 50/50 split, others 30/70, others stretch the installments differently. The percentages move around. The concept doesn’t: you pay part during construction, and the bulk at the end.

The detail most buyers miss: where your money actually goes

Here is the confusion worth clearing up, because mixing these two things up is the single most common mistake.

The money you pay during construction goes directly to the developer. There is no bank involved in that part. That capital is financing the construction of the building, and in exchange it buys your stake in the project. By the time the unit is delivered, that money is already “inside” the deal — it is your equity, your effective down payment on the finished property.

So when buyers ask, “what happened to the 50% I already paid?” — the answer is that it didn’t go anywhere. It’s not held by a bank, it’s not a loan, and it doesn’t get returned. It became your ownership stake in the property.

The balance at delivery: your two options

When the keys are ready and the final balance comes due, you have two ways to cover it.

Option 1 — Pay cash. You pay the remaining balance out of pocket, receive a clean title with no lien, and own the property outright with no debt.

Option 2 — Finance it with a Dominican mortgage. A DR bank lends you the remaining balance. This is where the earlier point matters: the bank does not touch the money you already paid the developer. That portion is already yours. The bank only finances the outstanding balance.

In practice, the bank appraises the finished property, confirms the equity you’ve already contributed, and lends the rest. For the bank, the amount you already paid during construction is your down payment. That’s why financing the back end of a pre-construction purchase is relatively comfortable for the lender: you’re asking to finance only part of a completed, delivered asset, which is a low loan-to-value loan. The more you paid in during construction, the stronger your position when you go to the bank.

How a Dominican mortgage actually works for a foreign buyer

A few realities change the numbers, and you should know them before you model anything.

Rates are higher than in the US or Puerto Rico. Mortgages in Dominican pesos generally carry double-digit rates; dollar-denominated mortgages, which some banks offer to foreigners, tend to run lower but still above what you’re used to in the US market. As of mid-2026, advertised rates from leading mortgage lenders ranged roughly from the high-8% area on promotional fixed terms up to around 13–14% depending on the bank, the term, and whether the rate is fixed or variable; dollar loans sat lower, in the ~8.5–11% range. Banks active in this space include APAP, Banreservas, Banco Popular, BHD, Scotiabank, and Promerica, among others. Treat any specific figure as a starting reference only — rates change constantly, so confirm the current number directly with two or three banks before you build it into a plan.

You can qualify as a foreigner, but with more requirements. Dominican banks do lend to non-residents. They typically finance a smaller share of the value (often up to somewhere in the 50–70% range) and ask for proof of income, references, and sometimes a local account. The process is slower and more document-heavy than what you’d expect in PR or the US.

Developer financing and bank financing are not the same thing. Some developers offer their own extended payment plan beyond delivery — that’s developer financing, usually short-term and on the developer’s own terms. A traditional bank mortgage is a different instrument with different rates and a different process. Ask which one you’re actually being offered.

Budget for the extra costs, not just the rate. A DR mortgage comes with closing costs beyond the loan itself: legal fees (around 0.4% of the price), appraisal, life and property insurance, and setup. Many banks also charge a prepayment penalty (commonly in the 2.5–3% range) if you pay the loan off early — which matters if you plan to sell or refinance before the term ends.

A worked example

Take a US$300,000 unit on a 50/50 plan:

- You pay roughly US$150,000 during construction — reservation, 20% at signing, then installments. This becomes your equity.

- At delivery, the remaining US$150,000 is due.

- If you pay cash: you own outright, no debt, clean title.

- If you finance: the bank treats your US$150,000 as a 50% down payment and lends the other US$150,000 — a 50% loan-to-value mortgage. Your monthly payment depends on the rate you’re quoted and the term, and your real return depends on that rate, your rental income, and your costs.

To see how the rate and the financing change your actual return, run the numbers in our [ROI Calculator] — the Advanced mode lets you enter your quoted rate, down payment, and closing costs and shows your cash-on-cash return and total ROI.

Frequently asked questions

Does the bank refund or take over the money I paid during construction? No. That money went to the developer and became your equity. The bank neither holds it nor counts it as part of the loan — it counts it as your down payment.

Can a foreigner get a mortgage in the Dominican Republic? Yes. You don’t need residency to buy, and banks lend to non-residents, typically financing a portion of the value with income proof and references. Expect a slower, more documented process than in the US.

Why is financing only the back half of the purchase easier for the bank? Because you’ve already contributed a large share of the value during construction, the bank is lending against a low loan-to-value on a completed asset — a lower-risk loan.

Are DR mortgage rates really higher than US rates? Yes. Peso mortgages commonly run in double digits; dollar mortgages are lower but still above typical US rates. Use the rate a Dominican bank actually quotes you, not a US assumption.

What’s the difference between developer financing and a bank mortgage? Developer financing is a payment plan offered by the developer, usually short-term and on its own terms. A bank mortgage is a separate, longer-term loan from a financial institution. Confirm which one you’re being offered.

Can I avoid a prepayment penalty if I sell early? It depends on the bank and the loan. Many DR mortgages carry a prepayment penalty (often 2.5–3%). If you expect to sell or refinance before the term ends, ask about this before you sign.

This guide is educational and describes general concepts, not financial, tax, or legal advice. Payment structures vary by developer; mortgage rates, foreign-financing limits, and bank requirements change over time and differ by institution. Verify current terms directly with Dominican banks and confirm your situation with a qualified Dominican attorney and accountant before committing funds.

About the author. Dr. Eduardo Santos-Alvarado is the researcher behind Punta Cana Investment Intelligence. A licensed real estate broker, he holds a Doctorate of Business Administration (DBA) with research focused on investor behavior in emerging tourism real estate markets. His work applies financial and consumer-behavior analysis to produce objective, verified intelligence on real estate investment in Punta Cana — not to sell property.

Related guides: What Is CONFOTUR? · Property Tax in the DR (the IPI), Explained · The Five Risks of Investing in Punta Cana Real Estate